Uniform Securities Act of 1956

- On the federal level, Investment Advisers are regulated by the investment advisers act of 1940

- On the state level, it’s the uniform securities act of 1956

- The exam is the property of the NASAA, or north american securities administrators association (nasaa)

- NOTE: If the question doesn’t specify, assume that the law to apply is state law.

TEST TOPIC ALERT

- General knowledge of the uniform securities act of 1956 and what it says is not enough for the exam. You need to be able to apply the law to concrete situations that may arise in the course of business

- The exam will often use the word administrator

Learning Objective 1: Define Investment Adviser

Any person who, for compensation, engages in the business of advising others, either directly or through publications of writings, as to the value of securities or as to the advisability of investing in, purchasing, or selling securities, or who, for compensation or as a part of a regular business, issues or promulgates analyses or reports concerning securities

- Definition of a person

- It’s also helpful to remember this as a three (3) prong test, as a person who:

- gives advice to others on securities

- does so as a part of regular business activity

- receives compensation for performing this activity

Giving Advice To Others on Securities

- This counts if the person provides advice about specific securities — stocks, bonds, mutual funds, limited partnerships as well as how to allocate assets among a group of securities. Even indirect advice is included here. This can also be written or oral

- e.g. “Why should you invest in XYZ?”

- e.g. “Here’s our view on future stock market trends”

- Note that advice on other investments is not advice about securities including: commodities, collectibles, precious metals, real estate.

In The Business of Providing Advice

- Giving advice on a regular basis is a business activity. It doesn’t have to be the principal activity of the person and frequency does matter, but is not the sole factor

- Advertises investment advisory services and presents himself as such.

- Note that any person whose business is to offer only nonspecific investment advice, through the publication of a general newsletter is not covered by the act (more on this later)

Compensation

- A person who receives any economic benefit (directly or indirectly through fees)

Investment Counsel

- Important definition investment counsel

SEC Release IA-1092

Learning Objective 2: Explain the impact of SEC Release IA-1092 on the definition of Investment Adviser and their activities.

- Since a bunch of people started offering investment advice in the 1980s, Congress told the SEC to define the activities that would subject a person to the investment advisers act of 1940. The SEC did this in the sec release ia-1092

Learning Objective 3: Identify exclusions and exemptions under the investment advisers act of 1940 and the uniform securities act of 1956

- Terminology is important and there’s a difference between exclusion from a definition and being exempt from a provision.

- Exclusion refers to not being included in a definition of a term as a whole. E.g. if a person is excluded from the definition of an Investment Adviser that person is not subject to provisions of state/federal laws that specifically refer to IAs. In other words, neither the investment advisers act of 1940 or uniform securities act of 1956 apply to those who are excluded here

- Exemption means not being subject to the registration of provision of the acts even though the person does meet the definition

Exclusions

-

There are 7 primary exclusions from the definition of an investment adviser

-

- Any bank and bank holding company, savings institution, or trust company — usually limited to US banks (unavailable to credit unions bank subsidiaries)

- definition bank holding company

- for the purposes here, the term “bank” does not include a savings/loan association or foreign bank, but does include a savings institution

-

- Any lawyer, accountant, teacher, or engineer whose advice is solely incidental to their practice of his profession is excluded - a.k.a. the L.A.T.E exclusion. This exclusion is not available to those who established a separate advisory business nmor those who hold themselves out as offering investment advice.

-

- Any broker-dealer whose performance of such services is solely incidental to the conduct of its business as a broker-dealer and who receives no special compensation (e.g. when offering wrap fee programs) is excluded. This also applies to registered representatives of broker-dealers

- definition broker-dealer

- definition wrap fee programs

the exclusion from the definition of investment adviser to broker-dealers is not in effect for those offering wrap fee programs - If asked what services are provided in a WFP, the correct choices would be investment advisory and __brokerage execution / transactions __ for a single “wrapped” fee. do not choose financial planning and recommendations

- smaller definition special compensation: compensation to the broker-dealer or salesperson in excess of that which he/she would be paid for providing a brokerage or dealer service alone.

-

- Publishers of nay bona fide newspaper, news magazine, or business or financial publications of general and regular circulation. I.e. 2 criteria must be met

- (a) publication must be general/impersonal in nature, in that the advice is not adapted to any specific portfolio

- (b) it also must be bona fide - or genuine - in that it contains disinterested commentary and analysis as opposed to promotional material

- (c) and it must be of general and regular circulation, in that it is not timed to specific market activity or events affecting, or having the ability to affect the securities industry

-

TEST TOPIC ALERT

- Note that an investment newsletter that is published for a subscription fee and rather than being published on a regular basis (weekly, monthly, etc.) issues are released in response to market events. The exclusion would be lost in this case

-

- Certain individuals who are employed by investment advisers, i.e. investment adviser representatives

-

- Any person who is a federal covered adviser is excluded

-

- Any other the administrator specifies is excluded.

- Publishers of nay bona fide newspaper, news magazine, or business or financial publications of general and regular circulation. I.e. 2 criteria must be met

Exemptions

- Exemptions are related to registering as an Investment Adviser (despite actually meeting the legal definition of one). These differ and are established on the federal and state level.

Federal Law Exemptions

- Intrastate Advisers: Only within one state. IAs, other than those who advise any private fund, whose clients are residents of the state in which the adviser has its principal office and only place of business and who do not give advice dealing with securities listed on any national exchange, are exempt.

- Advisers to Insurance Companies: IAs whose only clients are insurance companies are exempt

State Law Exemptions

- client-criteria exemptions: IAs, with no place of business in the state, are exempt from registering in the state provided their only clients in the state are

- registered broker-dealers

- other IAs

- institutional investors

- existing clients who are not residents but temporarily in the state

TEST TOPIC ALERT

- IA state registration exemption nuance for those who have

- no place of business in the state

- are licensed in another state

- offer advice in the state only with persons in the state who are already existing customers but are in the state “temporarily”

- This is sometimes called the snowbird exemption because it usually deals with people who spend winters in warmer places temporarily. No set time for what “temporary” means, but if the client changes their legal residence, that’s when this no longer applies

- The rules here are similar to having to register for a new license if you move to a new state (e.g. if you move states you have 30 days to get new stuff)

TEST TOPIC ALERT

- Understanding what constitutes a “place of business” is important for these exemptions

- if an IA advertises to the public in any way, the availability to meet prospective clients (hotel, country club, seminar, etc.), then they’re considered to have a place of business in the state

- But if an IA contacts existing clients who happen to be in the state and tells them they’ll be passing through and can meet up, they are not considered as having a place of business because it was not an announcement to the public only existing clients.

- limited to 5 or fewer clients (aka the de minimis exemption)

- any others the Administrator exempts by rule/order

- definition institution

- definition retail client

Learning Objective 4: Identify the exempt reporting adviser and private fund adviser exemptions

- (above exemptions) + below definition of private fund

Private Fund Advisers

- An overhaul to the registration process for investment advisers is contained in the private fund investment advisers registration act of 2010

- definition of private fund

Private Fund Adviser Exemption Under State Law

- mostly the same as the federal definition with two differences per the north american securities administrators association (nasaa)

- If qualifying for exemption under 3(c)(1), all investors must be “qualified clients” — i.e. have at least 2.1M net worth not including the value of primary residence

- Neither the private fund adviser or advisory affiliates are subject to “bad actor” provisions

Exemption for Foreign Private Advisers

- and IA that

- has no place of business in the US

- has fewer than 15 clients in the US in private funds

- has <$25M in AUM

- does not publicize themselves as an IA in the US

Exemption for IAs to VC Funds

- definition [[venture capital fund]]

- ## Learning Objective 5: Describe the investment adviser registration process, required post-registration filings, and business activities

- Unless an exemption is available, federal and state law make it unlawful for a person defined as an investment adviser to engage in advisory activity without registration

- registration is done on a federal or state basis - **never both**

Registration Requirements For IAs

- The national securities markets improvement act (nsmia) split registration requirements so that IAs wouldn’t have to register with both the SEC and the state, only one. They did this by creating a new definition - federal covered investment adviser

- Note that, when this happened, a bunch of states complained because they were losing state-revenue on the filings of some of the big fish that now would only register with the SEC. From this came a new fee the “notice filing” fee which required federally-covered advisers to give a copy of the SEC filing to the state and pay a fee

Dodd-Frank And Assets Under Management

- Large Investment Advisers: Those with at least 110 AUM

- Small Investment Advisers: IA with less than $25M, can’t register with the SEC unless they would need to register in 15+ states

- Mid-Size Advisers: between 100M AUM, must register with the state unless they (by law) can’t and want to register with the SEC instead, have to register in 15+ states, or take advantage of the buffer

-

Other Exceptions Under Dodd-Frank

- Some specific exceptions also apply that let others register with the SEC:

- pension consultants with at least $200M AUM (“significant enough to have an effect on national markets”)

- mid-size advisers with between 110M AUM

- investment advisers expecting to be eligible for SEC registration with 120 days of filing the application

- internet advisers

- Some specific exceptions also apply that let others register with the SEC:

The 20 Million Buffers

- State-registered already and have at least 110M, they can just register with the SEC anyway

- Since markets can fluctuate, and advisers shouldn’t need to switch back and forth, once you register with the SEC you’d only need to switch to being state-registered if AUM drops to 20M buffer”

Time for Measuring AUM

- AUM is reported annually by the IA, so the requirements to file or not to file with the SEC depend on that filing date and the value of the assets at that point in time. Fluctuations throughout the year wouldn’t trigger and changes (if for example a federally-covered IA fell below the required $90M AUM)

- There are three key times to remember:

- State-registered reports $110M+ they have to withdraw from the state and register with the SEC

- A new IA registering believes that it will have at least $100M in AUM within the first 120 days, it can just register for the SEC straight away

- SEC-registered IA reports <$90M in AUM, it has to withdraw and register with the appropriate states within 180 days

Registration Process

- A bunch of useless details summed up:

- Form ADV is what’s used to register/update IA registration

- Form ADV-W is what’s used to withdraw IA registration, this takes like 60 days

- it’ll ask about the firm itself (part 1) and who is a part of it (part 2) including who has control of the firm (above a certain % of voting power)

- what strategies are used can be found in Part 2A

- the form has to be updated each year within 90 days of the fiscal year

- there is some annual fee associated with updating the form

TEST TOPIC ALERTS

- There are no mimimum educational or experience requirements when filling out the form, but there is an area in the form where state-registered advisers have to identify execs and their formal education/business backgrounds

- Successor Firm: IF an IA changes its form of business organization (e.g. from sole proprietorship to corporation), a new form, but no fee is required

- Exempt Reporting Advisers (ERAs): If a private / venture capital fund that doesn’t need to register they still ned to file reports and fill out an abbreviated version of the first part of the Form ADV

Financial Requirements For Registration As An Investment Adviser

- Substantial Prepayment of Fees: To protect clients there are state and federal laws around IAs collecting “substantial prepayment of fees” based on $ amount and the contract period

- for a federal covered investment adviser, this is $1200+ and a 6+ month contract period

- for a state-registered IA, this is $500+ and a 6+ month contract period

- Balance Sheet Requirement for IAs: if an agreement requires a substantial prepayment, the agreement requires a balance sheet be included int he adviser’s ADV of the most recent fiscal year. It also must be audited by an independent public account. The same more or less applies to state-registered IAs (with the different definition of “substantial”)

- Disclosure of Financial Impairment: if you can’t meet contractual agreements as an IA and you either have a substantial prepayment or discretion/custody over client funds, you have to disclose any financial condition that could impair your ability to meet them.

TEST TOPIC ALERT

- An IA may be required to post a surety bond or maintain a minimum net worth if you either custody of funds or have discretion over a client’s account. For those with custody of funds the min net worth is 35K, for discretion over a client’s account it’s a min of $10K. If neither custody/discretion applies, but you still have a substantial prepayment of fees, then the IA must at least have a positive net worth

- Remember though that the uniform securities act of 1956is still only a template / model law, so individual states can have these numbers be higher

- Failure to Maintain Minimum Net Worth: Given the rules of custody/discretion/substantial fees, if an IA’s net worth falls below requirements, they have until the end of the next business day to file a financial report to the administrator and obtain a surety bond

- definition principal office

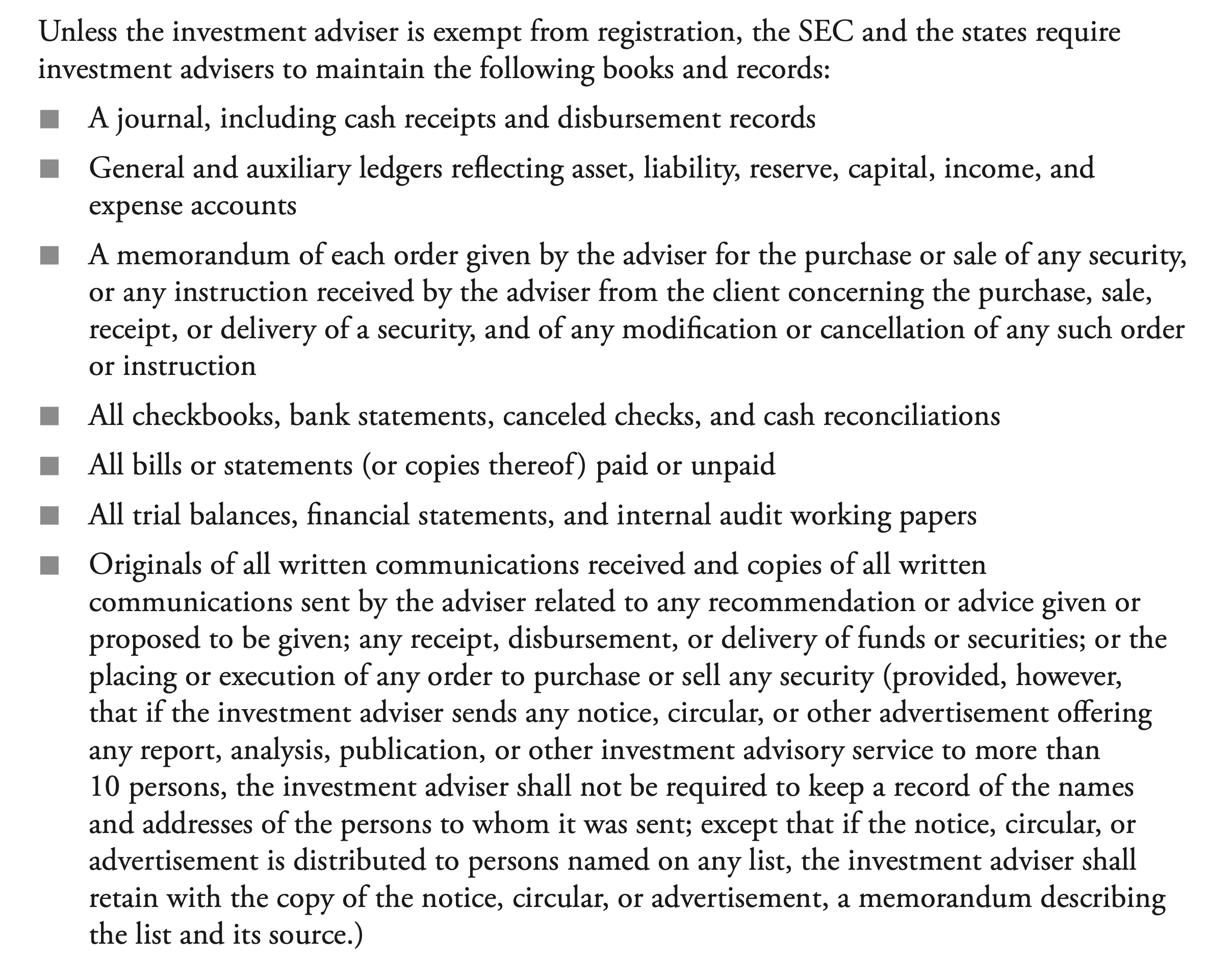

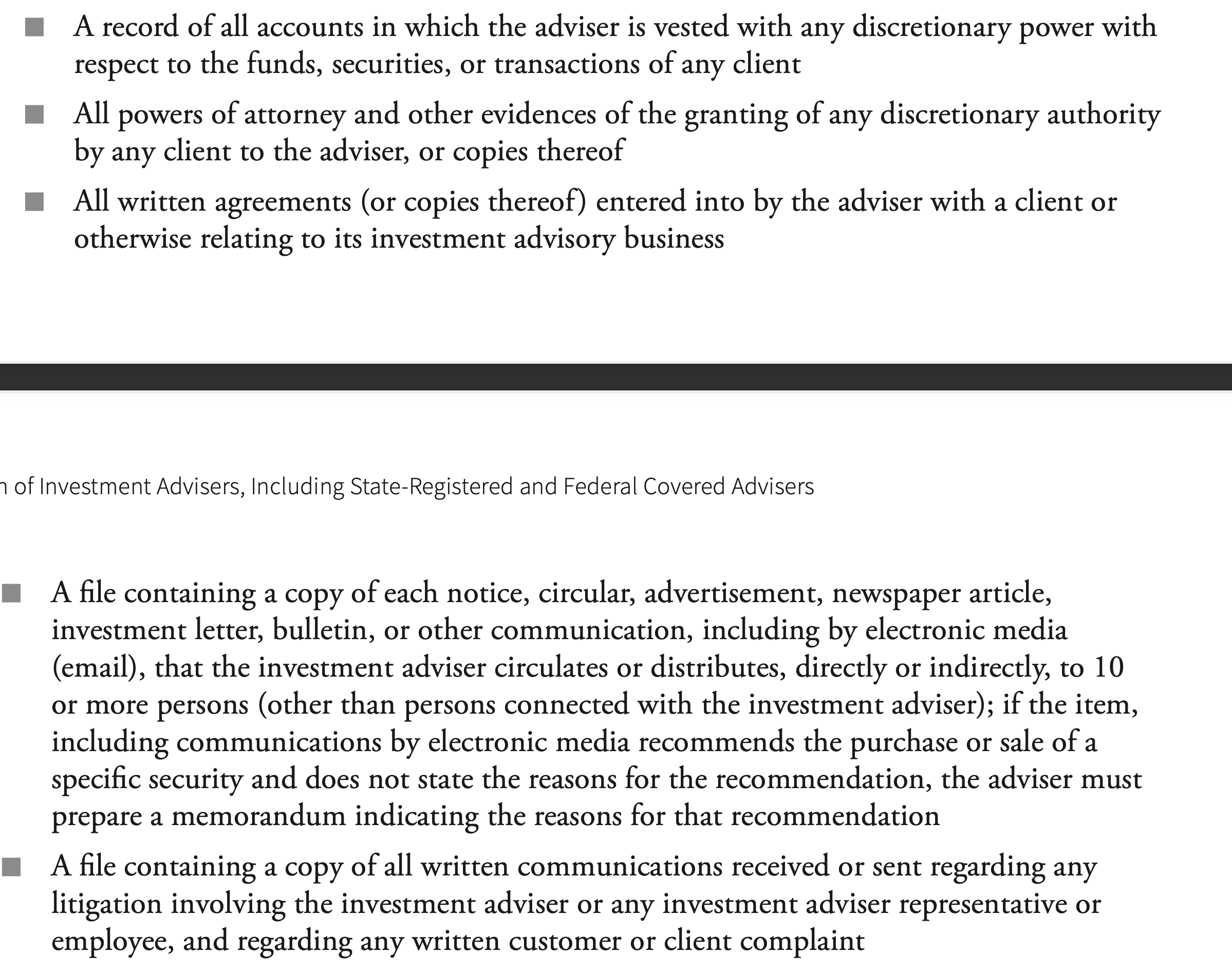

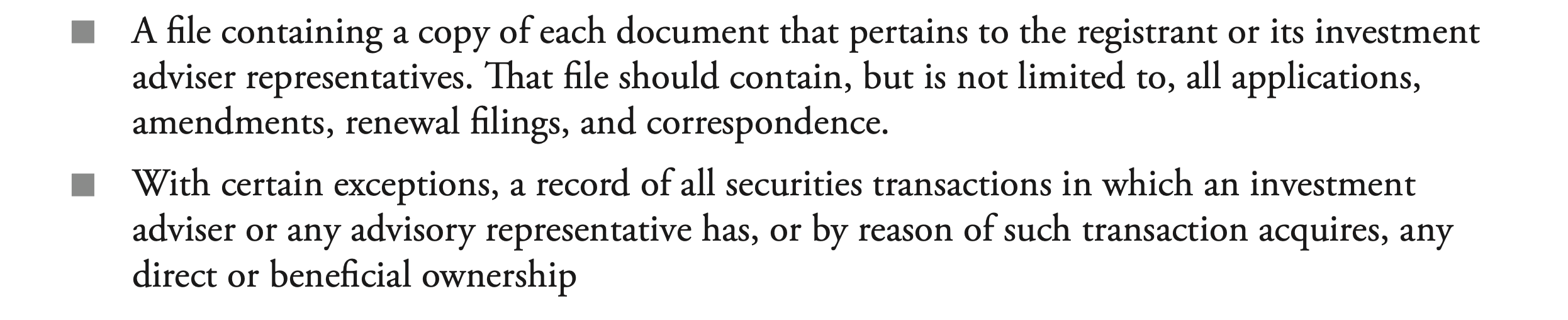

Books And Records Required By Federal And State Law